Business Reporter

Bank of England lowered interest rates for the second time this year - after years of mortgage costs and rising house prices, welcome news for first-time home buyers.

But it's still tough. According to real estate agent Savills, more than half of first-time buyers still rely on so-called mom and dad banks to go up the property ladder last year, with an average of £55,572 in loans and gifts last year.

We have talked to people about a range of revenues that have managed to push it to the ladder or on the verge of buying.

They shared with us their past buying strategies.

'We used the ISA for a lifetime'

Cameron Smith and Georgia Pickford, both 27 years old, each of whom opened a lifetime ISA (LISA) to buy a three-bedroom apartment in Hertfordshire last year for £320,000.

The scheme allows young people aged 18 to 39 to save up to £4,000 in government bonuses per year as long as it is used to purchase homes under £450,000.

Cameron made £40,000 and Georgia £37,000, each setting up a direct borrower to their respective Lisa accounts.

"Every month, my salary comes from my salary, no excuses, no distractions," Cameron said.

In less than three years, the couple saved £27,740, including their Lisas bonus. To achieve the full deposit amount, they earn this fee an additional £4,260 from their personal savings.

But Cameron said the plan did not keep up with the price increase.

“The cap of £450,000 is fixed in 2017 – it has not moved. If your property is even £1, you will lose the bonus and receive a 25% fine.”

Following the call from activists, the Finance Committee is reviewing whether the lifelong ISA is still suitable for purpose.

Brian Byrnes, head of personal finance at digital savings and investment platform MoneyBox, still sees the plan as a great choice for first-time home buyers.

"For the vast majority of customers, ISA's life is excellent. Less than 1% are affected by the £450,000 hat," he said.

“I used income to promote mortgages”

Abas Rai, 26, bought his first home with a £207,000 two-bedroom home in Suffolk using a joint mortgage called an income-promoting mortgage.

This is a product that some lenders offer that can add income from family members to your income even if they do not live in the property to increase how much you can borrow.

Even with a deposit of £30,000 and a salary of £33,000, Abas is still struggling to get the loan he needs. To increase his affordability, he added that his father (who made £24,000) had a mortgage.

By combining income, the bank is able to offer larger loans, although this means his father will also be held liable if his father defaults.

“Banks add up our income and multiply it by 4.5, and that’s how they address affordability.”

But involvement of parents poses some challenges.

“Because the property also adds people to mortgages, one of the risks is my father’s age – he is 55 and will retire soon, so if I default on payments, I will not be able to rely on his salary.”

Abas plans to remortgage and cancel his father once the income increases, but says the plan is worth it.

“If you don’t make money, say £45,000, you have someone in your family and I suggest you do it.”

“We moved to a cheaper area of 150 miles”

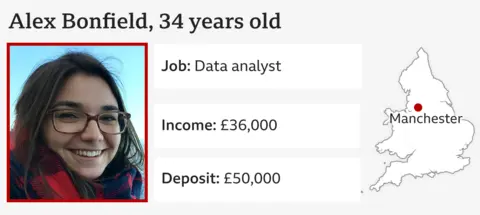

After years of renting in Oxfordshire, Alex Bonfield, 34, moved to Manchester to buy her first home.

"My wife is a teacher and she has to find a brand new job here. She really likes her old school, but it's more important," she said. "It's not an easy decision. We don't know anyone here."

The couple was purchased near family and friends in Oxfordshire, where the average house price is £479,000, while Manchester costs £251,000.

They started saving five years ago and are now hunting in the range of £300,000-325,000 with a deposit of £50,000.

“We are not the most important thing about our affordability, but we are very high.”

They are far from alone. According to Santander UK, 67% of first-time buyers have moved to the property ladder in the past two years.

"I'll share ownership and residence"

Oliver Jones, 27, lives in London and used a shared ownership plan to buy his first home - a two-bedroom apartment worth £500,000. He bought a 25% stake with a deposit of £40,000 and gave long-time friends he had rented out with in the past.

"We're tired of dancing every year, and landlords are trying to hike rent through stupid money," Oliver said. "Now, we're saving about £1,000 a month compared to our old apartment."

The shared ownership plan allows the buyer to purchase a portion of the property and the remaining rent. They are generally easier to access, but have complexities such as service charges and limited resale flexibility.

Oliver's total monthly fee is about £1,550, which includes a mortgage of £500, a 75% stake he does not own, and a £800 service fee. Oliver and his tenants informally allocate fees, covering all housing payments.

“My mortgage rate is 5.4%, but the unlimited portion of the rent is only 2% of the property’s value.

“It’s cheaper to own only a portion of the property and pay rent than to buy the whole thing with a big mortgage.”

“Buy ISA’s help for my work”

Daniel Price, 27, bought a three-bedroom home in the South Wales Valleys earlier this year, not far from growing up.

He began saving four and a half years using help from helping buy ISA - a government plan to increase savings by 25% to up to £3,000 in bonuses. Since then, it has been replaced by the ISA program.

"Initially, my mom told me about this, so I just put a pound into opening the account," he said.

“I paid £200 a month and ended up saving £11,000, which gave me a £2,500 government bonus.”

House prices in the South Wales Valley tend to be lower than in many other parts of the UK, which can make home ownership more accessible to first-time home buyers.

Daniel bought his house for £95,000, under the asking price of £110,000, due to some minor renovations required by the property.

“As a person, a lot of houses are out of my price range, so I started looking for a little further away.”

"My dad found the house on Rightmove and showed me the house. Everything is outdated, but it's still liveable. It just takes some work to modernize it."

When he first applied for a mortgage in October 2024, Daniel earned £18,000 a year while doing a software development apprenticeship. By the time of sales in January this year, his salary had risen to £24,000.

"When I was working as a warehouse manager at the factory, I started saving. Then, I worked as a technical apprenticeship and just finished. It helped me affordability."

“I bought a repairer –

Camilla de Cesare, 32, is a strategic consultant. She managed to buy her first home in London alone, but said it took seven years to live with her parents and was willing to buy a property that needed some work.

“My family helped me with my deposit, my job was stable, so I started with a lucky position,” she said.

Camilla saved £80,000 in the S&P 500, which tracks the performance of 500 leading companies listed in the U.S. stock market. By steadily contributing over time and benefiting from market growth, her investment pot eventually grew to £150,000.

“I’m really lucky that these S&P 500s have grown very well over the years I’ve invested in, so it provides me with a very healthy buffer.”

She spent a deposit of £50,000 and the remaining £100,000 will be renovated in the coming years, such as the new kitchen and bathroom.

She said it is easier to manage to save deposits when she can afford them.

"I think when you get the key for the first time, you just want to do everything right away. But looking around and knowing you've made something you've done, it's satisfying."

Tom Francis, head of digital consulting at financial adviser Money, said most people will benefit more from "slow, steady savings."

He encouraged potential buyers to divide their spending into three barrels: essentials, desires, and indulgence.

“Think of your dream home as a destination – you can’t get there if you don’t know where you start.”

Sarah Tucker, CEO of financial consulting firm The Mortgage Mum, urges young people not to wait until they save money before seeking financial advice from mortgage brokers.

“Even if you’re years after you’ve purchased, there’s nothing better than talking to a professional.”