AMD vs. Intel Stock: Better Semiconductor Turnaround Candidates

AMD vs. Intel Stock: Better Semiconductor Turnaround Candidates

While several chip stocks are convincing in 2024 Intel(NASDAQ:INTC) and Advanced Micro Devices(NASDAQ:AMD) Not among them. Intel shares are down about 60% last year, while AMD shares are down about 18%.

Let’s examine which semiconductor stocks look like better rebound candidates in 2025.

In a semiconductor market that is largely driven by artificial intelligence (AI), Intel and AMD are largely an afterthought. AMD is the distant designer of No. 2 graphics processing unit (GPU) after the market leader Nvidia. Meanwhile, Intel's market share in GPUs has dropped to zero, although the decline isn't far off, with the company having just 2% market share in PC graphics cards in 2023.

AMD has struggled with Nvidia, mostly due to its inferior software. In a recent study, Semianalyst called AMD's out-of-the-box GPUs “unusable” for AI training, noting that it would require “multiple teams of AMD engineers” to help it fix software bugs. However, AMD has been able to carve out a niche in AI inference, with Semianalyst saying its customers typically use AMD's GPUs for narrow, well-defined inference use cases.

Still, AMD was able to see strong data center growth, albeit not on the same scale as NVIDIA. Last quarter, its data center revenue grew 122%, while 25% revenue sequentially came in at $3.5 billion. The company attributed the jump in sales to its Instinct GPU and EPYC central processing units (CPUs).

The CPU acts as the brain of the computer, while the GPU has higher processing power. While there's a lot to like about GPUs, AMD has been doing well in the CPU market and noted that it's already doing well in the PC market, but it's already consistent in the CPU server market.

Overall, AMD's third-quarter revenue climbed 18% to $6.8 billion, and its adjusted earnings per share jumped 31% to $0.92. So, despite the decline in its stock price, the company is still growing well.

On the other hand, Intel's revenue fell 6% to $13.3 billion in the first quarter, and its adjusted earnings per share swung to -$0.46, compared with a profit of $0.41 a year ago. A bright spot last quarter was its data center and AI segments, where revenue grew 9% to $3.3 billion. However, compared to NVIDIA and AMD, this is a very modest gain in this segment.

Meanwhile, revenue in its largest segment, customer computing, fell 7% to $7.3 billion. By comparison, AMD's customer segment revenue rose 29% to $1.9 billion last quarter, suggesting it is having some impact on Intel's main PC business.

Perhaps Intel's biggest woes, though, stem from its foundry segment, which has been huge for its results. The company poured money into the business through capital expenditures (CAPEX) to build new manufacturing facilities. However, the segment has been a consistent currency loser, including reporting an operating loss of $5.8 billion last quarter, or a loss of $2.7 billion when excluding non-cash impairment charges.

Following the exit of its CEO Pat Gelsinger, Intel said it could divest itself of its foundry business. The business recently received $7.86 billion in direct funding, with the government receiving a 25% investment tax credit, to continue building its U.S. manufacturing footprint

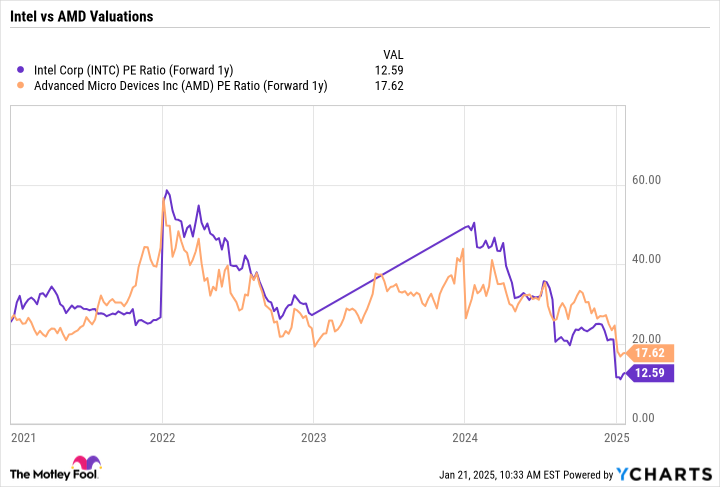

From a valuation perspective, Intel is a cheap stock, trading at a forward price-to-E ratio (P/E) of 12.6x compared to AMD's 17.6x.

YCHARTS's INTC PE ratio (forward 1 year) data.

However, if you value Intel's core business and its foundry business separately, its valuation becomes more attractive.

Intel's foundry business has been losing a lot of money, but it also has a lot of physical assets. Intel has spent $68.5 billion on CAPEX since the end of 2021, primarily on its foundry business, and has $100.4 billion in physical assets on its balance sheet. If you just take its recent capital expenditures and subtract its $26 billion in net debt, its foundry business would be worth about $1 billion, or $4.3 billion. It also owns 88% of the shares Mobileyeworth approximately $11.4 billion, or $2.66 per share.

So it's no surprise that the company has been the subject of takeover rumors. There's a lot of hidden physical assets that aren't reflected in its stock price, let alone direct government funding and tax incentives.

Meanwhile, AMD is certainly the stronger of the two businesses, even if it doesn't get the respect it deserves from investors. This could be a good place to start if more AI infrastructure turns to AI inference. At the same time, investors should not ignore its CPU business, which is gaining share in both data centers and PCs.

I like both stocks as turnaround candidates this year. I prefer Intel since I think there's still deep value in stock. However, AMD also looks like a solid rebound candidate. Fortunately, investors don't have to choose and can add both stocks to their portfolios.

Ever felt like you missed the boat on buying the most successful stocks? Then you will need to hear the news.

On rare occasions, our expert team of analysts publish “Double Down” Stock Suggest companies they think will be popular. If you're worried that you've missed the opportunity to invest, now is the best time to buy before it's too late. Numbers talking to themselves:

Nvidia:If you invested $1,000 in 2009 when it doubled,You will have $381,744! *

apple: If you invested $1,000 in 2008 when it doubled, You will have $42,357! *

Netflix: If you invested $1,000 in 2004 when it doubled, You will have $531,127! *

We're currently issuing “Double Down” alerts for three incredible companies, and there may not be another opportunity soon.

learn more”

*Stock Advisor returns as of January 21, 2025

Geoffrey Seiler has no position in any stocks mentioned. Motley Dummies has locations and recommendations for premium microdevices, Intel and Nvidia. The Motley Fool suggests the following options: Brief February 2025 $27 Intel Phone. Motley Fools has a disclosure policy.

AMD vs. Intel Stock: Better Semiconductor Turnaround Candidates originally published by Motley Fool